Introduction: The Shifting Balance of Power in the U.S. Housing Market

The U.S. housing market has undergone a dramatic transformation since the pandemic-fueled boom peaked in 2022. While sellers once held all the cards, the pendulum is slowly swinging back toward buyers — but not evenly across the country. Understanding where inventory is abundant or scarce is key to predicting price trends and negotiating power. This article examines the latest data on active listings and months of supply, revealing which states favor buyers and which still favor sellers.

Why Inventory Matters: The Connection Between Listings and Price Momentum

Active listings — the total number of homes for sale at a given time — serve as a critical barometer of market health. When inventory rises rapidly and homes sit on the market longer, sellers often face pressure to cut prices, signaling softening demand. Conversely, a sharp drop in listings, beyond normal seasonal patterns, gives sellers leverage to demand higher prices. Months of supply (the time it would take to sell all current listings at the current sales pace) is another key metric: a supply below 3 months typically favors sellers, while above 6 months favors buyers.

National Trends: Inventory Growth Slows but Remains Below Pre‑Pandemic Levels

As of April 2026, national active listings stood at 1,002,935, according to Realtor.com data. That represents a year-over-year increase of just 4.6% from April 2025, a significant deceleration from the 30.6% jump recorded the prior year. The slowdown suggests that the rapid improvement in buyer conditions may be leveling off.

Despite the recent uptick, inventory remains 11.8% below the pre-pandemic baseline of April 2019 (1,137,198 listings). The deficit is most pronounced in parts of the Midwest and Northeast, where supplies are still tight. In contrast, several Sun Belt states have seen listings surpass 2019 levels, leading to softer price growth or even declines.

Historical Inventory Snapshot (April 2017–2026)

The following numbers illustrate the dramatic impact of the pandemic and subsequent recovery:

- 2017: 1,198,424

- 2018: 1,102,064

- 2019: 1,137,198

- 2020: 941,733

- 2021: 435,663 (boom overheated)

- 2022: 379,978 (boom peak)

- 2023: 562,966

- 2024: 734,318

- 2025: 959,251

- 2026: 1,002,935

If the current pace of growth (about 43,684 additional listings per year) continues, we could reach roughly 1,046,619 by April 2027. This is not a prediction but a simple extrapolation of the trend.

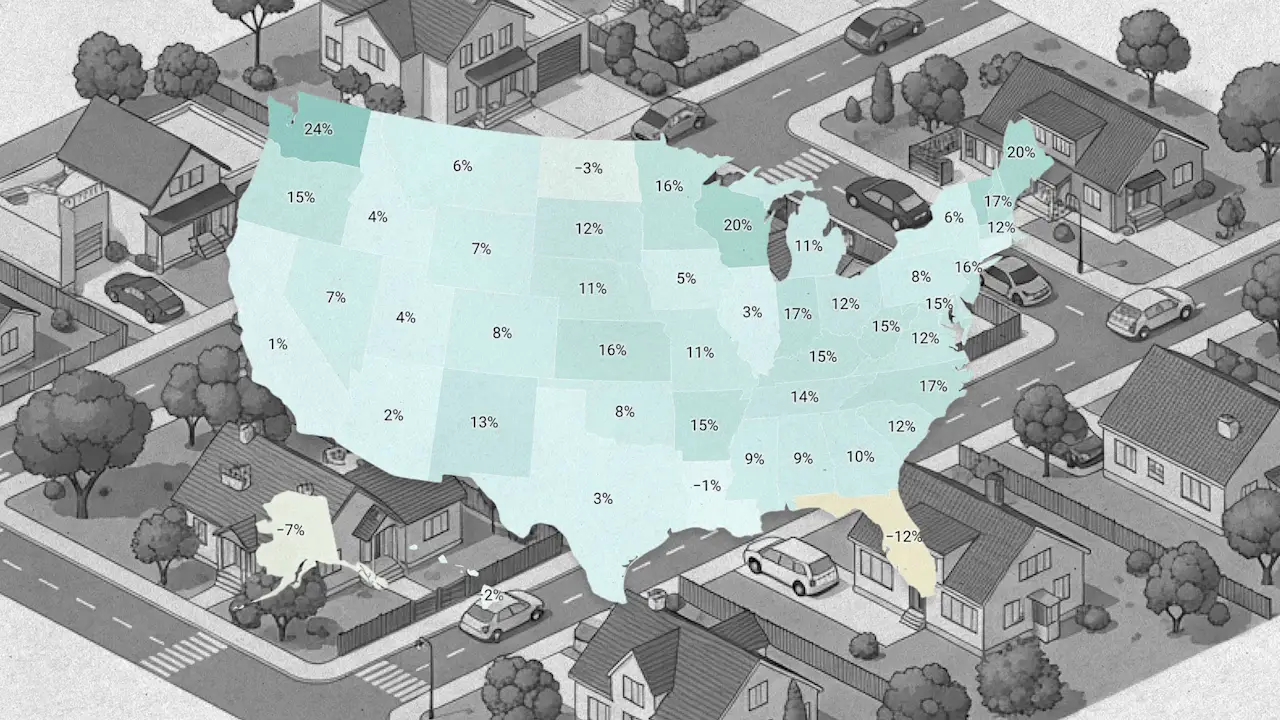

Regional Divide: Where Buyers Have Leverage vs. Where Sellers Still Rule

Nationally, the balance is shifting, but local conditions vary widely. As a rule of thumb:

- Markets with inventory above 2019 levels — often in the South and West — have experienced weaker price appreciation or outright declines over the past four years.

- Markets with inventory far below 2019 levels — especially in the Northeast and Midwest — have seen more resilient price growth.

States Where Buyers Have the Upper Hand

In states like Florida, Texas, and Arizona, active listings have surged well past pre-pandemic counts. This oversupply has softened price growth, giving buyers more negotiating room, longer decision times, and fewer bidding wars. For example, Florida’s inventory is up more than 30% from April 2019, according to the interactive chart (see the embedded Datawrapper visualization below for a full state-by-state breakdown).

States Where Sellers Still Dominate

Conversely, states such as New York, Massachusetts, and Minnesota still have inventory levels significantly below 2019. In these markets, multiple offers remain common, and sellers can often command prices above asking. The persistent shortage is due to a combination of factors: slow new construction, demographic demand, and homeowners reluctant to sell and give up low mortgage rates.

Looking Ahead: Will the Buyer’s Market Continue to Expand?

The national data suggests the gap between buyer and seller power is narrowing, but the overall equilibrium remains slightly tilted toward sellers. The recent slowdown in inventory growth could indicate that the market is stabilizing. However, if mortgage rates decline further or if more homeowners list their properties, supply could accelerate again, tipping the scales more firmly in favor of buyers. For now, prospective buyers should monitor their local inventory numbers closely, as conditions differ dramatically from one state — even one city — to the next.

For a detailed state-by-state comparison of year-over-year inventory changes, refer to the interactive chart below.